|

|

| COMPENSATION DISCUSSION AND ANALYSIS - TABLE OF CONTENTS |

|

| |

| |

INTRODUCTION | 25 |

|

EXECUTIVE SUMMARY | 25 |

|

Say on Pay | 25 |

|

| 26 |

|

| |

| 26 |

|

| | |

| |

|

| | |

| 31 |

|

| 31 |

|

| 33 |

|

Compensation Policies and Risk Considerations | 33 |

|

Relationship | 34 |

|

| | |

2014 | 35 |

|

| 35 |

|

| 36 |

|

| 36 |

|

| 39 |

|

| 42 |

|

| | |

| 42 |

|

| 42 |

|

| 42 |

|

| 43 |

|

|

| | |

| COMPENSATION TABLES | |

| | |

| |

| 44 |

|

| 45 |

|

| 45 |

|

| 46 |

|

| 46 |

|

| |

|

Employment Agreement and | 50 |

|

Termination Arrangement – NEOs (Excluding the CEO and President)CEO) | 53 |

|

| 54 |

|

Compensation | 56 |

|

|

|

| COMPENSATION DISCUSSION AND ANALYSIS |

INTRODUCTION

We will provide a detailed discussion of our executive compensation with a focus on the Compensation Committee’s decisions with respect to our NEO’s.NEOs. Our NEOs in 20142017 were:

|

| |

| NAME | POSITION |

Vincent D. Kelly Shawn E. Endsley

Colin M. Balmforth

Bonnie K. Culp-Fingerhut

Thomas G. Saine

| President and Chief Executive Officer |

| Hemant Goel | President, Spok, Inc. |

| Michael W. Wallace | Chief Financial Officer President, Spok, Inc.

|

| Thomas G. Saine | Chief Information Officer |

| Bonnie K. Culp-Fingerhut | Executive Vice President – Human Resource and Administration |

| |

| Former NEO | |

| Shawn E. Endsley | Former Chief InformationAccounting Officer |

EXECUTIVE SUMMARY

Say on Pay Results in 2017 and Stockholder Outreach

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 provides stockholders with a non-binding advisory vote (“Say on Pay”Say-on-Pay”) on the compensation of our NEOs as such compensation is disclosed in our annual proxy statement. We hold this votethese votes annually. In 2014,At our 2017 Annual Meeting, the 2016 NEO compensation program was approved by 94.2% of the votes cast, 52.0% voted againstshares voting (excluding abstentions and broker non-votes). Through our stockholder outreach in 2017 and through April 2018 we obtained feedback from our stockholders on our operational and financial performance as well as our NEO compensation on an advisory basis. In addition, the three directors on the Compensation Committee did not receive greater than 80% approval of the votes cast. In light of the results of the advisory vote, the Compensation Committeepay practices. This 2017 and management conducted2018 stockholder outreach to obtain feedback on our NEO compensation practices (and other corporate matters). This stockholder outreach involved:consisted of:

| |

| 1) | ContactingConducting quarterly reviews of our financial and operating results. For those stockholders who cannot attend the top 25 stockholders representing approximately 67%live meetings, we provide a recording of the total shares outstanding as ofreviews that can be accessed for 14 days subsequent to the date of record for the 2014 annual meeting. Representatives of the Compensation Committee and management met with 7 individual stockholders representing approximately 37% of the total outstanding shares of record. The remaining 18 stockholders either declined to meet with our representatives or did not return our inquiries.live meeting; |

| |

| 2) | Conducting anMeeting individually with investors or interested parties who request meetings with management to discuss our financial or operating results; |

| |

| 3) | Speaking with stockholders representing approximately 80.0% of our outstanding shares throughout the year; and |

| |

| 4) | An investor meeting for analysts and interested investorswas held at our Eden Prairie, MN office on November 20, 2014 in New York City.October 25, 2017. |

A more detailed discussion of our stockholder outreach is included in the section “Stockholder Outreach”"Stockholder Outreach" on page 30.29.

In response toBased on the stockholder outreachpast feedback from our stockholders, the Compensation Committee maderetained the following changes toelements previously established for our executive (including the NEOs) compensation practices:program:

| |

| 1) | Revised futureAwarded an annual LTIP awards to be made annuallyaward, which for a multi-year2017 50% was performance period as opposed tobased over a single award for one multi-year performance period; |

| |

| 2) | IncreasedRetained the CEO’sCEO's minimum stock ownership guideline to 3at three times the CEO’sCEO's annual salary; |

| |

| 3) | EstablishedRetained minimum stock ownership guidelines for all other executive officers (including all NEOs except the CEO)NEOs) at 1one times the executive officer’sofficer's annual salary; |

| |

| 4) | ProhibitedRetained the prohibition for hedging or pledging the shares of the Company's common stock by executive officers (including the NEOs) from hedging or pledging shares of the Company’s stock;; and |

| |

| 5) | Instituted aRetained the clawback policy regarding adjustment or recovery of compensation. |

The Compensation Committee added the following new element to our executive (including the NEOs) compensation program:

| |

| 1) | Awarded an annual LTIP award, which for 2017 50% was time based over a multi-year vesting period. |

Additional details can be found in section "Elements of Compensation" on page 31 as well as "Long-Term Incentive Compensation" on page 35.

Compensation Philosophy

The compensation philosophy of our Company is intended to motivate executives to achieve Spok’s strategic goals and operational plans and attract and retain high quality talent while the Company transitions from a wireless centric customer base to a growing software centric criticalhealthcare communications customer base. This philosophy is supported by an executive compensation program centered onincluding a pay-for-performance objective that aligns executive compensation with stockholder value.value as well as an equity interest in the Company which we believe aligns executive financial interests with those of our stockholders. That philosophy is translated into the executive compensation program design based on the following principles.

|

|

COMPENSATION PRINCIPLES Link all incentive portions of compensation to performance. We believe that compensation levels should reflect performance. This is accomplished by: • Motivating, recognizing, and rewarding individual excellence; • Paying short-term cash bonuses based upon Company financial performance; and • Linking elements of long-term compensation to our Company’s financial performance.performance coupled with preserving value through continued stewardship over time. Maintain competitive compensation levels. We strive to offer programs and levels of compensation that are competitive with those offered by companies of similar size, as well as our peer group, in order to attract, retain and reward our executives including the NEOs. Align management’s interests with those of stockholders. We seek to implement programs thatwhich will retain the executives while increasing long-term stockholder value by providing competitive compensation and granting long-term equity-based incentives. |

CEO Pay Ratio

The 2017 compensation disclosure ratio of the median annual total compensation of all Company employees to the annual total compensation of the Company’s chief executive officer is as follows:

|

| | | | |

| Category | | 2017 Total Compensation and Ratio |

| | | |

| Annual total compensation of Vincent D. Kelly, Chief Executive Officer | | $ | 2,769,082 |

|

| | | |

| Median annual total compensation of all employees (excluding Vincent D. Kelly) | | $ | 94,642 |

|

| | | |

| Ratio of the annual total compensation of Vincent D. Kelly, Chief Executive Officer as compared to the median annual total compensation of all employees | | 29.3:1 |

|

The calculation of annual total compensation of all employees was determined in the same manner as the Total Compensation shown for our CEO in the Summary Compensation Table. We identified the median employee by examining the 2017 total compensation for all individuals, excluding our CEO, who were employed by us on December 31, 2017. We included all employees, whether employed on a full-time, part-time, or seasonal basis; we did not make any assumptions, adjustments, or estimates with respect to total compensation, with the exception of annualizing the salary compensation for any full-time employees that were not employed by us for all of 2017.

Company Financial Performance

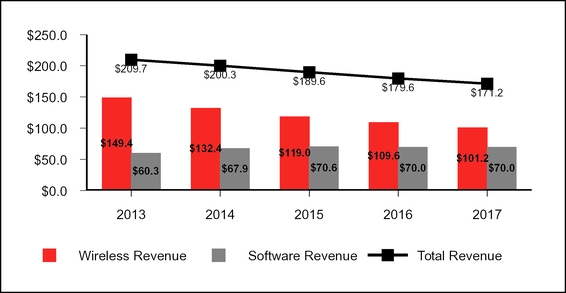

With the acquisition of the software operations in 2011 the Company has begun a long-term transition from a declining wireless centric customer base to a growing software centric criticalhealthcare communications customer base. This means that until our software revenue growth exceeds the decline in our wireless revenue, total consolidated revenue will decline.decline each year. Maintaining our position as a leader in healthcare communication and collaboration requires us to continue development of our integrated platform and invest in the key areas of customer need including: 1) mobility, 2) integrated platform, 3) nursing solutions and 4) alerting. We will continue to increase our spending on product development and strategy in 2018 and beyond to develop these solutions and compete in the changing marketplace. This also means that operating cash flow (a non-GAAP financial measure)investment in our future has been and will alsobe reflected in our research and development expenses. The Company is not aware of any specific event which was the primary cause for a decline year over year until the Company successfully transitions to growth. Both consolidated revenuein share price between January 1 and operating cash flow (as defined by the Company), along with software bookings, have been identified by the Compensation Committee as key drivers of stockholder value during this transition.December 31, 2017.

In order to facilitate this transition we established our 2014The 2017 operating objectives and priorities thatestablished for the Company which were outlined in our 20132016 Annual Report.Report to Stockholders reflect this transition. Our achievement against these operating objectives and priorities is outlined below.

|

| |

20142017 Operating Objectives and Priorities | 20142017 Achievement |

| |

1)Grow Growth of our software revenue and bookings. | Annual software revenue remained flat compared to 2016, but software operations bookings grew to 115.8% of 2016 software operations bookings. |

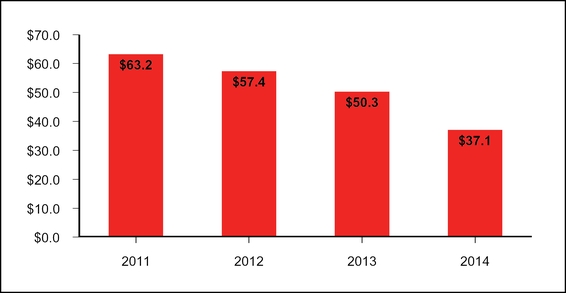

2)Retain Retention of our wireless subscribers and revenue stream. | Net churn for wireless subscribers in 2017 was 5.6% versus 5.3% in 2016. Wireless revenue declined 7.7% in 2017 versus a decline of 7.9% in 2016. |

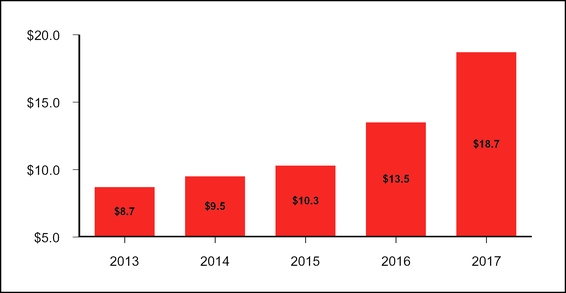

| 3) Invest in our future solutions. | Research and development expenses increased by 38.9% to $18.7 million in 2017. |

| 4) Return capital to our stockholders. 4)Seek long-term revenue growth through business diversification.

| 1)Annual software revenue grew 12.5% over 2013. Software operation bookings grew 28.5% over 2013.

2)Net Churn for wireless subscribers in 2014 was 8.7% versus 9.2% in 2013. Wireless revenue declined 11.4% in 2014 versus a decline of 11.3% in 2013.

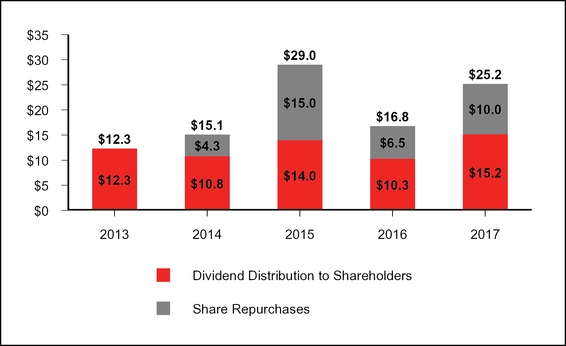

3)Cash dividends paiddeclared in 20142017 were $10.8$10.3 million and common stock repurchases were $4.3$10.0 million.

4)

|

| 5) Long-term revenue growth through business diversification. | We investigated potential acquisition candidates but did not identify any candidates that met our screening criteria to provide stockholder value at a reasonable valuation. |

We also announced our plan to return $26 million to stockholderscontinue our regular quarterly dividend of $0.125 per common share in 2015 through a combination of dividends, common stock repurchases and/or special dividends.2018.

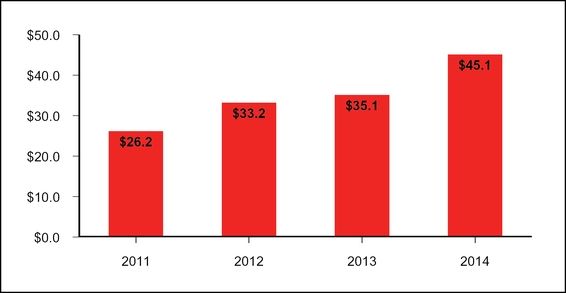

The following graphs provide a summary of the Company’s annual financial performance sinceover the acquisition of the software operations in March 2011. This summary also includes our 2014 achievements which support the Company’s long-term transition from a declining wireless centric customer base to a growing software critical communications customer base.

The following financial performance measures cover the fourfive year period ended December 31, 2014 and demonstrates the Company’s performance2017 during the long-term, ongoing transition from a declining wireless centric customer base to a growing software centric criticalhealthcare communications customer base. These financialThe research and development expense changes illustrate our investment to develop our healthcare communications platform and invest in the key areas of customer need including 1) mobility, 2) integrated platform, 3) nursing solutions and 4) alerting. The wireless revenue, software operations bookings, and adjusted operating and capital expenses performance measures have beenare used by the Compensation Committee as performance criteria for the annual2017 short-term incentive plan (“STIP”).

REVENUE

(IN MILLIONS)

CONSOLIDATED OCF*

(IN MILLIONS)

|

|

| RESEARCH AND DEVELOPMENT EXPENSES |

| ($ IN MILLIONS) |

|

|

ADJUSTED OPERATING AND CAPITAL EXPENSES(1) |

| ($ IN MILLIONS) |

(1) Adjusted Operating cash flow (“OCF”) is defined as operating income plusand Capital Expenses exclude severance, depreciation, amortization and accretion, less capital expenditures. (All determined in accordance with U.S. Generally Accepted Accounting Principles, (“GAAP”.) OCF is a non-GAAP measure used as a measure of free cash flow.

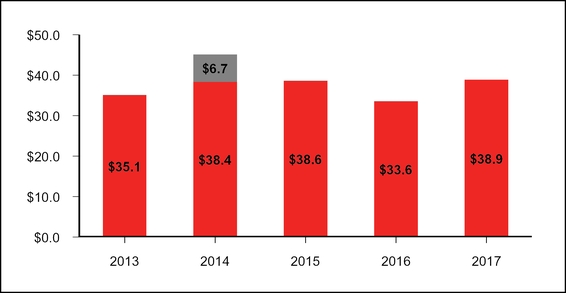

SOFTWARE OPERATIONS BOOKINGS*

(IN MILLIONS)

|

|

SOFTWARE OPERATIONS BOOKINGS(1),(2) |

| ($ IN MILLIONS) |

(1) Software operations bookings represent contractual arrangements to provide software licenses, professional services and equipment sales. These contractual arrangements (bookings) represent future revenue.

| |

| (2) | Software operations bookings in 2014 reflect $6.7 million in federal government activity that was not replicated in subsequent years. |

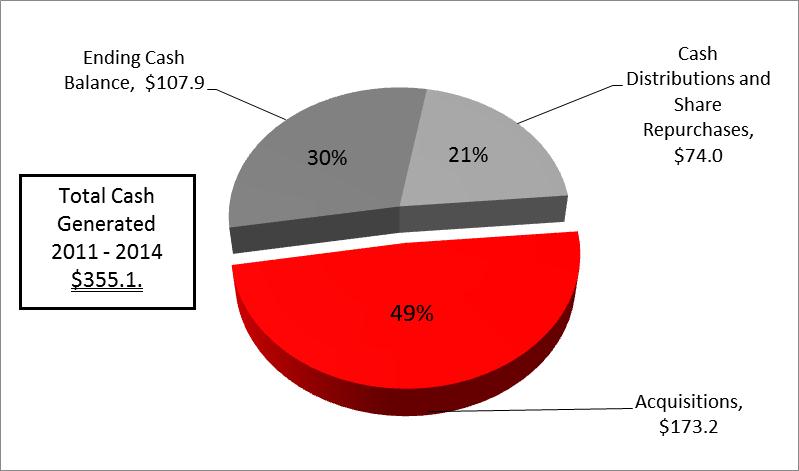

FREE CASH FLOW ALLOCATION

(2011-2014 $ IN MILLIONS)

|

|

| CASH RETURNED TO SHAREHOLDERS |

| ($ IN MILLIONS) |

STOCKHOLDER OUTREACH

On an annual basis the compensation of our NEOs, as such compensation is disclosed in our annual proxy statement, is submitted to our stockholders for a non-binding advisory vote (“Say on Pay”).Say-on-Pay vote. In 2014, 52.0%2017, the 2016 NEO Compensation Program was approved by 94.2% of the votes cast voted againstshares voting (excluding abstentions and broker non-votes). We believe that the significant support for the NEO Compensation Program was due in part to the continuing impact of the elements outlined below which were implemented in recent years, but we also continued our stockholder outreach in 2017 and through April 2018 to obtain feedback from our stockholders on our operational and financial performance as well as our NEO compensation on an advisory basis. In light of the results of the advisory vote the Compensation Committeepay practices. This 2017 and your management conducted a2018 stockholder outreach program to discuss and obtain feedback on our NEO compensation and other corporate matters.

For this stockholder outreach we:consisted of:

| |

| 1) | ContactedConducting quarterly reviews of our financial and operating results. For those stockholders who cannot attend the top 25 stockholders representing approximately 67%live meetings we provide a recording of the total shares outstanding as ofreviews that can be accessed for 14 days subsequent to the date of record for the 2014 annual meeting. Seven (7) individual stockholder meetings were held representing approximately 37% of the total outstanding shares of record. The remaining 18 stockholders either declined to meet or did not respond to our inquiries, andlive meeting; |

| |

| 2) | ConductedMeeting individually with investors or interested parties who request meetings with management to discuss our financial or operating results; |

| |

| 3) | Speaking with stockholders representing approximately 80% of our outstanding shares throughout the year; and |

| |

| 4) | Holding an investor meeting for analysts and interested investorsat our Eden Prairie, Minnesota office on November 20, 2014 in New York, New York.October 25, 2017. |

For this stockholder outreach the individual investor meetings the Chair of the Compensation Committee, the CEO, the CFO and the Corporate Secretary and Treasurer attended. The agenda for the meetings requested feedback from stockholders and generally included the following additional content depending on the requests from the individual stockholder: (1) a review of the Company’sCompany's operations and results to date, (2) a discussion of the Company’sCompany's strategic direction outlining the Company’sCompany's transition from a declining wireless revenue base to a profitable growing criticalhealthcare communications software business and (3) a reviewany other matters that were of interest to investors including the Company’sCompany's compensation philosophy, long-term stockholder value, and its alignment with the Company’sCompany's strategic direction. In some casesDuring 2017, the Company spoke directly with stockholders representing approximately 80% of the total shares outstanding as of December 31, 2017. The Company did not receive any significant feedback on corporate governance matters. Generally, the CEO, was excused from the compensationCFO, the Corporate Secretary and Treasurer and our investor relations professionals took part in these discussions with individual stockholders. In respondingand our stockholders were free to feedback on the Company’s compensation philosophy the Chairmake inquiries about any matter of the Compensation Committee described the elements of the Company’s compensation (see page 33).

Discussion of Performance Criteria – The Chair of the Compensation Committee also described the Compensation Committee’s rationale for the selection of the performance criteria for both the STIP and long-term incentive plan (“LTIP”). Given the Company’s long-term transition from a declining wireless revenue base to a growing critical communications base, the Compensation Committee determined that a focus on consolidated revenue, OCF (as defined by the Company) and software bookings would focus management on the key metrics supporting the generation of long-term stockholder value during the transition. Several stockholders inquired asinterest to the Compensation Committee’s consideration of Total Shareholder Return (“TSR”) or Return on Invested Capital (“ROIC”) as compensation performance criteria. The Chair of the Compensation Committee acknowledged that TSR or ROIC were possible metrics; however, the Compensation Committee believed that TSR and ROIC were short-term oriented and that management should be focused on profitably guiding the Company to sustainable growth during this transition period. The Compensation Committee believed the identified criteria appropriately motivated management.stockholder.

Compensation Practice Changes – Based on the stockholder feedback the Compensation Committee made the following changes to executive officer (including the NEOs) compensation practices:

| |

1) | Revised future LTIP awards to be made annually for a multi-year performance period as opposed to a single award for a multi-year performance period; |

| |

2) | Increased the CEO’s minimum stock ownership guideline to 3 times the CEO’s annual salary; |

| |

3) | Established minimum stock ownership guidelines for all executive officers (including all NEOs except the CEO) at 1 times the executive officer’s annual salary; |

| |

4) | Prohibited executive officers (including the NEOs) from hedging and pledging shares of the Company’s stock; and |

| |

5) | Instituted a clawback policy regarding adjustment or recovery of compensation. |

Selected stockholders also provided the Company with their views on Board diversity and Board tenure which was conveyed to the Nominating and Governance Committee.

EXECUTIVE COMPENSATION DESIGN

Objectives

The design of our executive compensation has been made to considerprogram reflects the unique strategic situation of the Company using the compensation principles of our Compensation Philosophy. Our Company has been a public company since we were founded in November 2004 resulting from the merger of Metrocall Holdings, Inc. and Arch Wireless, Inc., the two largest remaining independent paging companies in the United States. The merger allowed us to consolidate operations, reduce costs and create stockholder value including the return of $492.5$98.4 million throughbetween January 1, 2013 and December 31, 20142017 in the form of dividendscash distributions (including dividends) and common stock repurchases. This merger also allowed for management of the declining wireless customer base to focus on the most profitable industry segments, primarily healthcare.

In an effort to capitalize on the valuable customer franchise from our wireless customer base in the healthcare industry segment, we acquired Amcom Software, Inc. (“Amcom”) in 2011. Amcom provided criticalhealthcare communication software solutions to customers in a variety of industries with a particular emphasis on healthcare. This common focus on the healthcare segment provided our Company with a unique opportunity. ThatThis unique opportunity allowed for transition from a declining wireless revenue stream to a growing criticalhealthcare communications software business while creating significant stockholder value during the transition. In essence, the Company must profitably manage two revenue lines: 1) a declining wireless revenue stream and related subscribers and 2) a growing criticalhealthcare communications software business. We are engaged in a multi-year transition from a declining hardware based wireless company to a growing criticalhealthcare communications software company. Becoming the leader in healthcare communication and collaboration requires us to continue development of our integrated platform and invest in the key areas of customer need including: 1) mobility, 2) integrated platform, 3) nursing solutions and 4) alerting. We will continue to increase our spending on product development and strategy in 2018 and beyond to develop these solutions and compete in the changing marketplace. These strategic considerations are important operational elements considered by the Compensation Committee in determining 20142017 compensation for our executives, including our NEOs. The Compensation Committee actively considers the implications of this business transition and the evolving size and nature of the overall business when developing the target pay opportunities as part of the executive compensation program design.

For all of our executives, which include the NEOs, incentive compensation in 2017 is intended to be based on the operating performance of the Company as a whole as determined by the Compensation Committee and ratified by the Board. The Compensation Committee believes that elements of incentive compensation paid to executives should be closely aligned with the Company’s short-term and long-term performance; linked to specific, measurable results thatwhich create value for stockholders; and assist the Company in attracting and retaining key executives critical to long-term success.

In establishing compensation for executives, the Compensation Committee has the following objectives:

Attract and retain individuals of superior ability and managerial talent;

Ensure compensation performance criteria are aligned with our corporate strategies, business objectives and the long-term interests of our stockholders through profitable management of our transition;

Achieve key strategic and financial performance measures by linking incentive award opportunities to attainment of performance criteria in these areas; and

Focus executive performance on long-term stockholder value, as well as promoting retention of key staff, by providing a portion of total compensation opportunities in the form of direct ownership in our Company through performance-basedperformance, and time-based, RSUs thatwhich are payable in our common stock when such RSUs vest.

Prior to establishing the compensation plans, the Board and the Compensation Committee reviews with management the Company’s long range plan (“LRP”). The following table highlights certainLRP is a five year projection of ourthe Company's operations. This LRP was reviewed with the full Board at two meetings during the year. The Board discusses with management the Company’s operational priorities, strategic direction, budget assumptions including headcount, sales, research and development spending, capital expenditures, revenue growth, subscriber churn, maintenance retention and other elements supporting the LRP. The Board also reviews a detailed narrative which encapsulates this process. The Board takes great care in setting compensation plans, including determination of performance criteria, to ensure plans are robust, compensation is adequately proportioned between cash and equity in order to create both short term stability and long-term focus. The Board and Compensation Committee actively and independently considers the performance criteria and management projections when determining the appropriate performance criteria for use in Short-Term Incentive Compensation ("STIP") and Long-Term Incentive Compensation ("LTIP") as the basis for motivating executive compensation practicesperformance.

Based on this understanding of the Company’s operations and plans, as detailed in the LRP, the Compensation Committee identified all key performance criteria, as further outlined under the Short-Term and Long-Term Incentive Compensation sections, that, drivein the judgment of the Compensation Committee, would support the Company’s capital allocation and long-term stockholder value creation plans. The Compensation Committee believes that the selected performance as well as those not implemented because we do not believe they would serve our stockholders’ interests.criteria for both the STIP and LTIP incentive management to weigh its operational decisions in a manner that best supports the interests of stockholders.

|

| |

What We Do | What We Don't Do |

üTie pay to performance by ensuring that all incentive plans for all executives, including NEOs, are performance based and at risk for 2014. 58% of CEO compensation was performance based and at risk.

üProvide termination and change-in-control agreements to all executives, including NEOs for retention and continuity in the case of a change-in control.

üProvide only minimal perquisites.

üRequire stock ownership of all Executives, including NEOs and directors.

üProhibit hedging and pledging of our stock for all executives and directors.

üProvide long-term incentive compensation that is 100% performance-based in the form of RSUs payable in common stock only upon the achievement of measurable pre-established performance criteria.

üProvide caps on potential payment of both short-term and long-term incentives with clawback provisions.

| ×Do not have employment contracts with executives, at this time, except for agreements with our Chief Executive Officer and President that evidences their long-term commitment to the Company.

×Do not provide excise tax gross-ups.

×Do not provide significant additional benefits to executives that differ from those provided to all other employees.

×Do not pay dividends on any unvested long-term incentive equity awards (“RSUs”). Dividend equivalent rights (“DERs”) are only payable on such RSUs to the extent the RSUs ultimately vest and are earned.

|

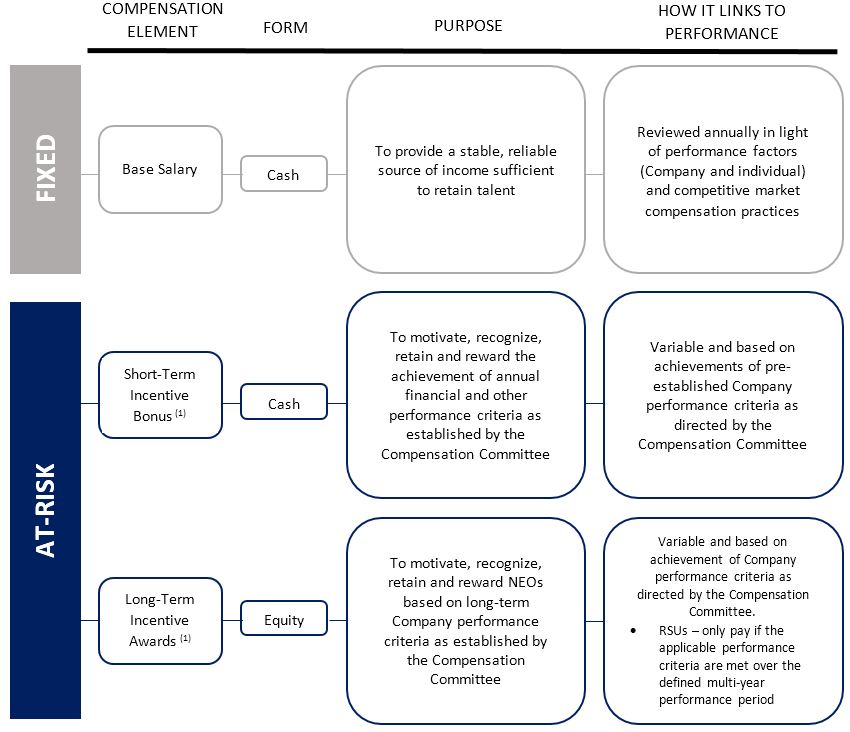

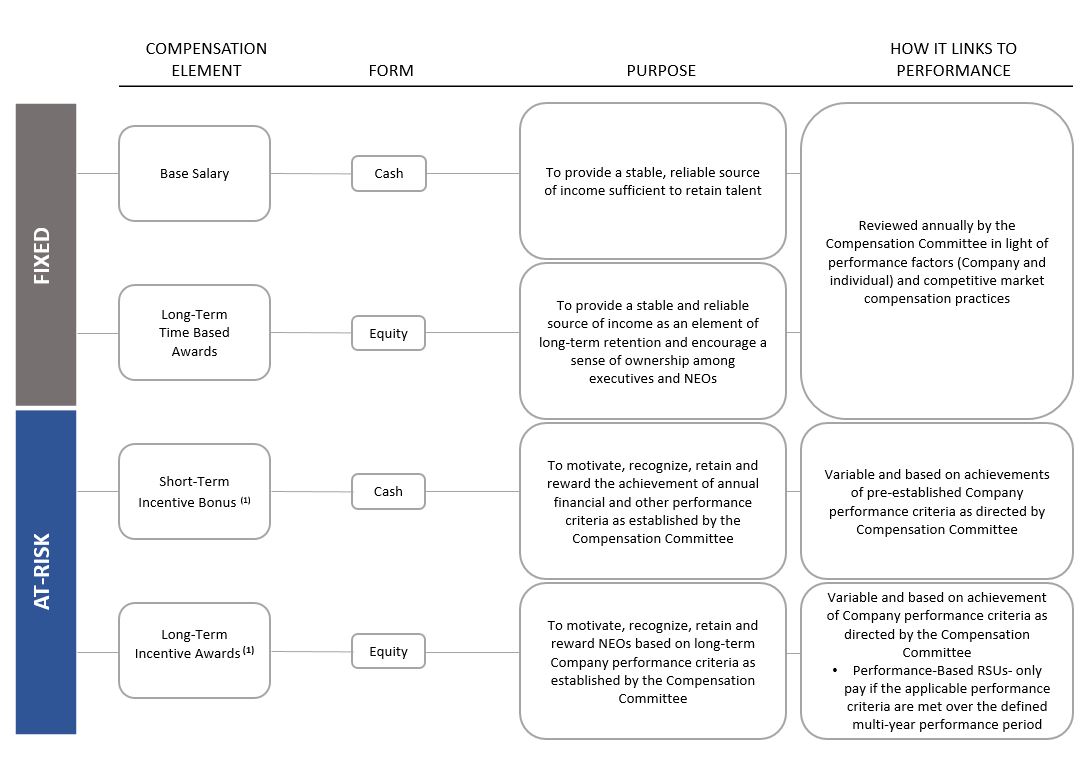

Elements of Compensation

The following chart summarizes the key pay elements during 2017 for our executives including the NEOs. Each element is described in detail beginning on page 3533 in the section “2014“2017 Executive Compensation Program Decisions”.

| |

| (1) | The “At-Risk” compensation elements are based on incentive plans approved in advance by the Compensation Committee. The 2017 STIP was 50% financial performance and 50% operational performance based while the LTIP was 25% financial performance, 25% operational performance and 50% time based. Both the performance based STIP and LTIP provideawards provided for non-payment or caps on potential payment of the awards if the pre-established performance criteria are not met or exceeded. Both the performance based STIP and LTIP provideawards provided that if certain pre-established performance minimums are not met, no payment is made.made on the performance based components. |

Compensation PoliciesWe believe, given the industry in which we operate and Risk Considerations

The Board, through the corporate culture that we have established, base compensation, cash bonuses and equity incentives at levels consistent with those for executives, including NEOs, of comparable companies are generally sufficient to retain our existing executive officers and to hire new executive officers when and as required. Our Compensation Committee applies the same compensation policies and practices to allbelieves a significant portion of our executives, including NEOs, compensation should be tied to our performance.

We believe, as is common in the NEOs. The two at-risk elements oftechnology sector and with our executive compensation program are the STIP and the LTIP awards. With respect to both the STIP and LTIP awards, the Compensation Committee establishes measurable performance criteria that is based on company-wide metrics such as consolidated revenue, OCF (defined as operating income plus depreciation, amortization and accretion, less capital expenditures; all determined in accordance with U.S. GAAP) and operations bookings (sales

orders from customers for our software solutions). Determination of the payouts for the STIP and LTIPindustrial peers, equity awards are measured against the pre-established Company-wide criteria. The Compensation Committee believes that this approach focuses eacha key compensation-related motivator in attracting and retaining executive on overall measurable Company performance, minimizes the riskofficers in addition to base salary and cash bonuses. Each of conduct detrimental to the Company and retains the executive. these components are discussed in further detail in later sections.

The Compensation Committee also established policies that prohibitedwhich prohibit executives, including the NEOs, from hedging or pledging their shares of the Company’s common stock andstock. In addition our Compensation Committee has instituted a clawback policy regarding adjustment or recovery of compensation. Such policies will also amelioratereduce risks associated with the Company’s compensation policies. We believe that our compensation policies and practices are not likely to have a material adverse impact on the Company.

Relationship with Compensation Consultants and Use of Peer Groups

In response toGiven the strong approval of our negative advisory Say-On-Pay results in 20142016 Executive Compensation Program, the Compensation Committee engageddetermined that minimal changes would be made to the form, amounts and structure of the 2017 Executive Compensation Program, although, in accordance with our peers, the program was changed in 2017 to implement annual RSU awards which are time-based (with a three-year vesting period) under our LTIP. Additional information regarding the time-based RSU awards can be found beginning on page 37. The Compensation Committee determined that compensation consultants Hay,did not need to assist the Compensation Committeebe engaged in evaluating the executive compensation of the NEOs as well as the Company’s compensation policies. Hay was engaged to perform an assessment of executive compensation focused on:

Competitiveness of the2017 for overall executive compensation program relative to a proxy peer group on a target basis;

Pay mix (the weighting between base salary, short-term and long-term incentives) for the NEOs relative to the peer group; and

Prevalence of long-term incentive vehicles and practices within the peer group as well as the type of long-term incentives.

Hay reported directly and exclusively to the Compensation Committee and worked with members of our management only on matters for which the Compensation Committee is responsible. Moreover, Hay did not perform any other services for, or receive any other fees from, our Company or any of our subsidiaries other than in connection with the assessment of NEO compensation. As required by Item 407(e)(3)(4) of Regulation S-K and the NASDAQ listing standards, the Compensation Committee has considered certain factors relating to the Hay’s independence and has determined that its work has not given rise to any conflict of interest. Total fees paid to Hay in 2014 were less than $100,000.

Peer Group – The peer group consists of twenty similarly situated companies in both the wireless and software industries which represented a competitive market for executive talent, business and capital. Information from this peer group was used to assess NEO compensation for 2014.

The following peer groups was approved by the Compensation Committee (for use by Hay):

|

| |

•Consolidated Communications Holdings, Inc.;

• NTELOS Holdings Cop.;

• Iridium Communications Inc.;

• Alaska Communications Systems Group, Inc.;

• Cogent Communications Holdings, Inc.;

• Shenandoah Telecommunications Company;

• Atlantic Tele-Network, Inc.;

• Medidata Solutions, Inc.;

• CalAmp Corp.;

• Merge Healthcare Incorporated;

| •

Computer Programs and Systems, Inc.;•

magicJack VocalTec Ltd.;•

Meru Networks, Inc.; and•

Vocera Communications, Inc. |

Hay analyzed both the elements and amounts of executive compensation for the NEOs in comparison to executive compensation in the peer group. Based on this analysis Hay recommended no changes to the elements of executive compensation (base salary, short-term incentive and long-term incentive). Hay determined that target total cash compensation (base salary plus short-term incentive compensation) was generally competitive with the peer group findings for all NEOs. In addition, Hay provided the Compensation Committee with recommendations on the form and amount of long-term incentives for all NEOs.design. The Compensation Committee revieweddid not engage in benchmarking or utilize a peer group in making its decisions regarding the recommendations of Hay and took them into consideration for purposes of 2015 NEO compensation.2017 Executive Compensation Program.

2017 EXECUTIVE COMPENSATION PROGRAM DECISIONS

The elements of compensation, all of which are discussed in greater detail below, include:

Base Salary;

All Other Compensation;

Short-Term Incentive Compensation;

Long-Term Incentive Compensation; and

Termination and Change-in-Control Arrangements.

Base Salary

Base salaries are intended to provide our NEOs with a degree of financial certainty and stability that does not depend on our performance, and are part of the total compensations package that the Compensation Committee believes is necessary to help ensure the retention of our NEOs. The base salary element of our compensation program is designed to be competitive with compensation paid to similarly situated, competent and skilled executives.

As noted earlier, Based on the Company’s planned operations for 2017, the Compensation Committee engaged Hay toCommittee's review bothof the elements and amounts of executive compensation for NEOs. After considerationprogram and the overwhelming approval by stockholders of Hay’s recommendationsthe 2016 Executive Compensation Program the Compensation Committee made no changes to the NEO base salaries.salaries for 2017.

The base salaries paid to our NEOs are set forth in the Summary Compensation Table on page 4441 in the Salary column.

35 The increase in salary in 2015 reflects a one time extra biweekly payroll payment due to the payroll leap year. All employees of the Company received this extra biweekly payroll payment.

All Other Compensation

We provide certain employee benefits and limited perquisites to our NEOs. In general except as noted below, the other elements of compensation are the same as offered to all other employees of the Company.

Perquisites – We provide a car to the CEO pursuant to his employment agreement.

Insurance Premiums – We paid for basic life insurance at the value of the NEO’s annual salary to a maximum of $250,000. This is available to all employees of the Company.

Company Contribution to Defined Contribution Plan – All Company employees are eligible to receive a Company contribution.

Spok Holdings, Inc. Savings and Retirement Plan (the “Plan”) is open to all Company employees working a minimum of twenty hours per week with at least thirty days of service. The Plan qualifies under Section 401(k) of the Internal Revenue Code (the “Code”). Under the Plan, participating employees may elect to voluntarily contribute a percentage of their qualifying compensation on a pretax or after-tax basis up to the annual maximum amounts established by the Code. The Company matches 50% of the employee’s contribution, up to 5% of each participant’s gross salary per pay period, or 50% of the employee’s annualized contribution up to $2,500, whichever is greater. There is a per-pay-period match on the 5% component and an end-of-year true up on the $2,500 component. Contributions made by the Company become fully vested three years from the date of the participant’s employment. Profit sharing contributions are discretionary. In 2014, 20132017, 2016 and 2012,2015, we made matching contributions in amounts equal to $29,387, $25,135$29,229, $32,971, and $17,990,$31,565, respectively, for the NEOs participating in the Plan as reflected in “All Other Compensation Table for 2014”2017” in the “Compensation Tables” section on page 45.42.

Dividend Equivalent Rights (“DERs”) – Participants in the 20112015 LTIP, including the NEOs, wereare entitled to accrue DERs on each RSU granted to the participant. Each DER representedrepresents the value of dividends paid on the Company’s common stock during the 20112015 LTIP performance cycle. In 2014 the performance cycle for the 2011 LTIP was completed and the targeted awards were earned and the vested RSUs were paid in common stock of the Company in 2015. In addition, eachcycles. Each participant, including the NEOs, wasis entitled to receive in cash the DERs accrued on

the underlying RSUs. Payment ofRSUs if the DERs was made to each participant, including the NEOs, in 2015.pre-established performance criteria is met. If a participant voluntarily leftleaves the employ of the Company, the underlying DERs wereare forfeited along with forfeiture of the unvested RSUs.

Other Employee Benefits – We maintain broad-based benefits for all employees, including health, vision and dental insurance, disability insurance, paid time off and paid holidays. Executives (including NEOs) are eligible to participate in all of the employee benefit plans on the same basis as other employees with the exception of increased vacation accrual and eligibility for payout of that vacation accrual at time of termination.

Short-Term Incentive Compensation (“STIP”)

Our STIP is designed to motivate our executives and key employees (including the NEOs) and reward them with cash payments for achieving quantifiable, pre-established Company performance criteria.

Corporate Summary – From the formationDescription of the Company in 2004 through 2011 the Company managed a declining wireless centric customer base that was characterized by declining consolidated revenue. Despite that declining revenue the Company had increased margins, provided steady cash dividends and made common stock repurchases. Starting in 2011 with the acquisition of Amcom the Company initiated a long-term transition from a declining wireless centric customer base to a growing critical communications software centric customer base. Until the software revenue growth exceeds the decline in our wireless

revenue, total consolidated revenue will decline year over year. This also means that OCF (a non-GAAP financial measure) will also decline year over year until the Company successfully transitions to growth.

Prior to establishing the performance criteria for the STIP both the Board and the Compensation Committee reviews with management the Company’s long range plan (“LRP”). The LRP is a five year projection of the Company operations. (In 2013 the LRP covered the years 2014-2018.) This LRP was reviewed with the full Board at two meetings during the year. The Board discusses with management the Company’s operational priorities, strategic direction, budget assumptions including headcount, sales, capital expenditures, revenue growth, subscriber churn, maintenance retention and other elements that support the LRP. The Board also reviews a detailed narrative that encapsulates this process. The Board takes great care in setting performance criteria to ensure the performance criteria is robust and long-term focused. The annual budget for 2014 from which the STIP performance criteria are established results from the LRP.

During the transition period the Compensation Committee understands that the Company’s key performance criteria such as consolidated revenue and OCF will be lower than the prior year reflecting the strategic nature of the Company’s business. The Compensation Committee has established a higher performance level in 2014 for operations bookings as this performance criteria is focused on transitioning to the software centric portion of the customer base. Based on this understanding of the Company’s operations and plans as detailed in the LRP, the Compensation Committee identified the key performance criteria for the 2014 STIP that, in the considered judgment of the Compensation Committee, would support the Company’s capital allocation and long-term stockholder value creation.

STIP Performance Criteria – Based on the information from the LRP for 20142017, the Compensation Committee approved the performance criteria of the 20142017 STIP on December 6, 2013 to be effective January 1, 2014.2017. The 20142017 STIP was payable in cash, based upon separate pre-established performance criteria which included totaladjusted consolidated operating and capital expenses, wireless revenue, software operations bookings, and development milestones, each of which is measurable and readily reportable and requires the coordination and cooperation of all of management for achievement. The Compensation Committee chose adjusted operating and capital expenses to replace adjusted operating cash flow in order to provide focus on the individual components that adjusted operating cash flow is derived from. Additionally, the Compensation Committee replaced total consolidated OCF.revenue with wireless revenue to ensure attention was placed on both the wireless and software revenue streams (software bookings).

The Compensation Committee selected the 2017 performance criteria, all of which are key elements leading to long-term stockholder value creation, for the STIP based on the following rationale:

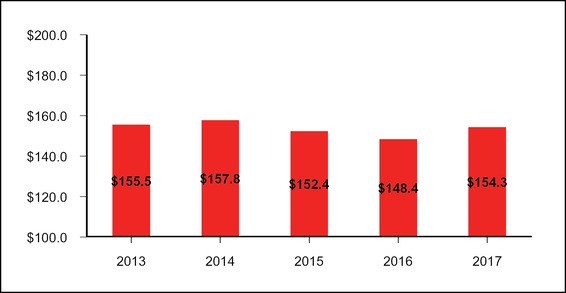

ConsolidatedAdjusted Operating and Capital Expenses – Adjusted Operating and Capital Expenses is defined as operating expenses less depreciation, amortization and accretion expense, less severance, less stock based compensation, plus capital expense (all calculated in accordance with U.S. GAAP). This performance criteria is a non-GAAP measure of the companies operating expenses. This performance criteria measures the Company’s ability to manage its operations expenses based on parameters established by the Board.

Wireless Revenue – As noted earlier, the Company is in transition from a declining wireless centric revenue base to a growing software centric base as represented by software revenue. The Company’s operations requireAs the Company transitions to a software centric base, the Compensation Committee believes it is important to focus on both typesthe retention of revenue. Untilwireless revenues to continue internal funding of research and development projects which it anticipates will fuel long term growth. A short-term focus on retention of the Company accomplishes itswireless revenue stream will in turn provide for the present endeavors within our research and development function and our continued transition to overall growth thisinto a software centric business. This performance criteria will necessarily reflect a reduction in revenue in comparison to actual results from the prior year. The performance criteria is measurableyear given the declining nature of revenues related to those products and focuses management on both a declining wireless revenue stream and a growing software revenue base. This performance criteria is readily reported and requires the coordination and cooperation of all management. The Compensation Committee believes this is a key element of stockholder value creation.services.

Software Operations Bookings – Software operations bookings represent contractual arrangements to provide software licenses, professional services and equipment sales. These contractual arrangements (bookings) represent future revenue. This performance criteria is measurable and focuses management on supporting the critical drivers for future growth and implementation of the transition to growth. This performance criteria is readily reportable and requires the coordination and cooperation of all management. As the Company accomplishes its transition to overall growth, this performance criteria will generally reflect an increase from the prior year. year based on the Compensation Committee's understanding of the Company's operations. In establishing the software operations booking target level for 2017 the Compensation Committee reviewed the actual performance level for software operations bookings in 2016 and set the 2017 target performance level higher than actual performance in 2016.

Development Milestones: Prototype Platform and Alpha/Beta Delivery - as noted earlier, one of our Operating Objectives is to invest in our future solutions. This has resulted in Project Catapult which is designed to integrate our existing solutions, together with physician and nursing workflows, into a seamless platform of healthcare communication and collaboration. Given the planned increase in research and development expenditures for 2017 to achieve this goal, it was critical to establish specific development milestones to measure the progress of Project Catapult. As such, two criteria were established: 1) Prototype Platform - validation of the Company’s physician based secure messaging direction, solution and scope, through guided demonstrations of a working commercial prototype to existing hospital customers who agreed to participate as Innovation Partners with representation from physicians, nursing and technology; and 2) Alpha/Beta Delivery - delivery of both alpha and beta versions of the Prototype Platform to such Innovation Partners during 2017.

The Compensation Committee believes this is a key elementassigned the greatest weight to the timely completion of our research and development efforts as it measures the Company's ability to deliver growth and long term stockholder value creation.

Consolidated OCF – OCF is defined as operating income plus depreciation, amortizationin alignment with the Company's long term vision through the creation and accretion expense, less capital expense (all calculated in accordance with U.S. GAAP). This performance criteria is a non-GAAP measuredeployment of the free cash flow available to stockholders for dividends, stock repurchases,

acquisitionsnew software products and investments in the business. This performance criteria measures the Company’s ability to manage its operations profitably based on parameters established by the Board. Until the Company accomplishes its transition to overall growth this performance criteria will reflect a reduction from the prior year. This performance criteria is measurable and readily reportable and requires the coordination and cooperation of all management for achievement. The Compensation Committee believes this is a key element of stockholder value creation.services.

The Compensation Committee believes that these three 2014five 2017 STIP performance criteria are the key elements that supportsupporting stockholder value creation and appropriately focusedfocus management on successfully transitioning the Company to growth.

Performance Criteria Establishmentlevels are based on the Company's transition - During the transition period, the Compensation Committee understands that the outcomes of certain of the Company's key performance criteria, such as wireless revenue, will be lower than the prior year reflecting the strategic nature of the Company's business. The Compensation Committee has established a higher performance level in 2017 for software operations bookings as compared to actual 2016 software operations bookings (see "Description of the STIP Performance Criteria" above) as this performance criterion is focused on transitioning to the software centric portion of the customer base.

Payouts are determined by interpolation of performance goals – Straight-line interpolation is used to determine payouts for STIP awards when 1) the actual performance is between the threshold performance targetlevel and target performance level andor 2) the actual performance is between the target performance level and the maximum performance target.level. There is no STIP payout if achievement is below the threshold performance target.level. Payments under the STIP are contingent upon continued employment, though pro rata payments will be made in the event of death or disability based on actual performance at the triggering event date relative to targeted performance measures for each program. Further, if an executive’s employment is involuntarily terminated (other than for cause), the executive will be eligible to receive a pro rata payment of the STIP for the year of termination, subject to the execution of an appropriate release and other applicable and customary termination procedures.

The threshold, target and maximum performance goals for each component of the performance criteria and the payouts that would have been provided under the 20142017 STIP in the event of performance at each applicable level are set forth in the following tables.

|

| | | | | | | | |

Performance Criteria(2) | Relative Weight | | Threshold Payout Against Target | Threshold Performance Level (In 000s) | Target Payout | Target Performance Level (In 000s) | Maximum Payout Against Target | Maximum Performance Level (In 000s) |

OCF(1) | 50% | | 75% | $28,432 | 100% | $35,540 | 125% | $42,648 |

| Consolidated Revenue | 25% | | 70% | $175,325 | 100% | $194,806 | 130% | $214,286 |

| Operations Bookings | 25% | | 75% | $35,406 | 100% | $39,340 | 125% | $43,274 |

| Total | 100% | | 73.75% | | 100% | | 126.25% | |

|

| | | | | | | | |

Performance Criteria(1) | Relative Weight | | Threshold Payout Against Target | Threshold Performance Level (In 000s) | Target Payout | Target Performance Level (In 000s) | Maximum Payout Against Target | Maximum Performance Level (In 000s) |

Adjusted Operating and Capital Expenses(2) | 15% | | 80% | $193,306 | 100% | $161,088 | 125% | $128,870 |

| Wireless Revenue | 10% | | 80% | $77,483 | 100% | $96,854 | 130% | $106,539 |

Software Operations Bookings(3) | 25% | | 80% | $28,000 | 100% | $35,000 | 150% | $38,500 |

Development Milestone: Prototype Platform(4) | 25% | | 0% | — | 100% | 4/30/2017 | 100% | 4/30/2017 |

Development Milestone: Alpha/Beta Delivery(4) | 25% | | 0% | — | 100% | 12/31/2017 | 100% | 12/31/2017 |

| Total | 100% | | 40% | | 100% | | 119.25% | |

| |

| (1) | OCF is calculated as operating income plus depreciation, amortization and accretion less purchases of property and equipment (all determined in accordance with U.S. GAAP). |

| |

(2) | The Compensation Committee selected the performance criteria as key measures in determining stockholder value. The relative weight assigned to each performance measure reflects the judgment of the Compensation Committee as to the importance each measure has to stockholder value. |

| |

| (1) | Operating expenses less depreciation, amortization and accretion expense, less severance, less stock based compensation, plus capital expense (all calculated in accordance with U.S. GAAP). |

| |

| (3) | Software operations bookings represent contractual arrangements to provide software licenses, professional services and equipment sales. These contractual arrangements (bookings) represent future revenue. |

| |

| (4) | Target dates are an all or nothing performance objective. Failure to complete the required research and development tasks prior to the established deadline results in no payout on the related criterion. |

The Compensation Committee actively considers the appropriate size of the pay opportunity each year in light of the evolving nature and size of the business. The Compensation Committee determines the threshold, target and maximum payouts for each performance criterion based on the Compensation Committee's understanding of the Company's LRP and the expectations for 2017. Based on this understanding the Compensation Committee also establishes the relative weighting for each performance criteria with Development Milestone afforded the most significant weighting (see "Description of the STIP Performance Criteria").

In establishing the software operations booking target level for 2017 the Compensation Committee reviewed the actual performance level for software operations bookings in 2016 and set the target performance level higher than actual performance for 2016.

Then the Compensation Committee established the threshold and maximum payout levels based on the Compensation Committee's judgment as to the impact on stockholder value.

The amounts paid under the 20142017 STIP were based on the following achievement against the pre-established performance criteria.

|

| | | | |

| Performance Criteria | Relative Weight | Actual Performance (in 000s) | Actual Payout | Weighted Actual Payout |

| OCF | 50% | $37,149 | 106.8% | 53.4% |

| Consolidated Revenue | 25% | $200,273 | 111.2% | 27.8% |

| Operations Bookings | 25% | $45,408 | 125.0% | 31.3% |

| Total | 100% | | | 112.5% |

|

| | | | |

| Performance Criteria | Relative Weight | Actual Performance (in 000s) | Actual Payout | Weighted Actual Payout |

| Adjusted Consolidated Operating and Capital Expenses | 15% | $154,254 | 106.4% | 16.0% |

| Wireless Revenue | 10% | $101,188 | 117.9% | 11.7% |

| Software Operations Bookings | 25% | $38,912 | 150.0% | 37.5% |

| Development Milestone: Prototype Platform | 25% | Completed | 100% | 25.0% |

| Development Milestone: Alpha/Beta Delivery | 25% | Incomplete as of 12/31/2017 | —% | 0.0% |

| Total | 100% | | | 90.2% |

The STIP for each NEO is based on a percentage of the NEO’s base salary. For the NEOsNEOs' 2017 STIP, the percentage of base salary, the targeted payout and the actual payout were as follows:

| | | NEO | STIP Percentage of Base Salary | Targeted Payout ($) | Actual Payout ($) | STIP Target Opportunity - Percentage of Base Salary | Targeted Payout ($) | Actual Payout ($) |

| Vincent D. Kelly | 100% | 600,000 | 675,000 | 100% | 600,000 | 541,200 |

| Shawn E. Endsley | 75% | 187,500 | 210,938 | |

| Colin M. Balmforth | 75% | 262,500 | 295,313 | |

| Hemant Goel | | 100% | 350,000 | 315,700 |

Michael W. Wallace(1) | | 75% | 262,500 | 181,636 |

| Thomas G. Saine | | 75% | 206,250 | 186,038 |

| Bonnie K. Culp-Fingerhut | 75% | 151,939 | 170,931 | 75% | 168,750 | 152,213 |

| Thomas G. Saine | 75% | 206,250 | 232,031 | |

(1)Actual payout based on pro-rated service in 2017 from March 27, 2017.

Long-Term Incentive Compensation (“LTIP”)

Our 2017 LTIP rewards eligible executives, including the NEOs, through a combination of equity awards that contained time-based vesting and vesting based on the future financial performance of our Company by providing equity awards for creating value for our stockholders.Company. The goals of our long-term incentive program are to:

EnsureTo reinforce a sense of ownership and to align the financial interests of eligible executives, including the NEOs, financial interests are aligned with those of our stockholders interests;stockholders;

Motivate decision making thatdecision-making which improves financial performance of our criticalhealthcare communications business over the long-term particularly during thisthe Company's transition;

Recognize and reward superior financial performance of the Company; and

Provide a retention element to our compensation program.

These goals were used in establishing the 2011 LTIP performance criteria outlined below.

No additional long-term incentive compensation was granted in 2014 to eligible executives including the NEOs as 2014 was the final year in the four year performance period for the 2011 LTIP. The details on the 2011 LTIP are2017 grant outlined below.

20112017 LTIP AWARDSAWARD – VESTED ON DECEMBER 31, 2014; PAID IN 2015 – On March 15, 2011, theThe Compensation Committee adopted andapproved the Board ratified the 20112017 LTIP forwhich was granted to eligible employees, including NEOs, based on performance criteria established by the Compensation Committee for the Company. During 2011 and 2012, our NEOs, other than Mr. Balmforth, participated in a prior long-term incentive program, the 2009January 2017. The 2017 LTIP

which vested based on a performance cycle through December 31, 2012. Beginning in 2013 (or upon his hiring in 2012 for Mr. Balmforth) our NEOs commenced participation in the 2011 LTIP.

The 2011 LTIP provided grants provide eligible employees the opportunity to earn long term incentive compensation based on continued employment with the Company and the Company’s attainment of certain financial goals as determined by the Compensation Committee and set forth in the 2011 LTIP duringfor the period from January 2, 2011 and1, 2017 through December 31, 2014 for the wireless operations and April 1, 2011 and December 31, 2014 for the software operations (collectively the “performance2019 (the “2017-2019 performance period”).

Management recommended and the Compensation Committee, in its sole discretion, selected employees to be participants in the 2011 LTIP and, in its sole discretion, determined the target awards that were earned by each 2011 LTIP participant.Time-Based Vesting Awards - The Compensation Committee determined target awards based on a multipleit would be appropriate and in the best interest of the 2011 STIP targetCompany and its stockholders to award for each participant (or, with respecta portion of its equity awards as time-based vesting to participants selectedencourage, retain, and reinforce a sense of ownership among executives, including NEOs. The Company anticipates future equity incentive awards will continue to participatebe awarded as a combination of both time, and performance-based, awards, however, the Compensation Committee may also consider other alternative forms of equity-based awards in the 2011 LTIP after the commencement of a performance period, the STIP target award for the year in which the participant commenced participation in the 2011 LTIP) orfuture.

In January 2017, as otherwise determined bydescribed above, the Compensation Committee.

Under the terms of the 2011 LTIP,Committee awarded time-based RSUs to eligible employees, including NEOs. 100% of the target award is made in the form of RSUs granted under our 2004 and 2012 Equity Plans,Plan, subject to vesting as described below. (The 2004 and 2012 Equity Plans are fully described in our 2014 Annual Report.) Awards granted prior to May 16, 2012 were granted pursuant to our 2004 Equity Plan and awards granted on or after May 16, 2012 were granted pursuant to our 2012 Equity Plan. Additionally, participants are entitled to DERs with respect to the RSUs to the extent that any cash dividends or cash distributions (regular or otherwise) are paid with respect to our common stock during the vesting period. Vested RSUs will be settled in the Company's common stock and vested DERs will be paid in a lump sum cash payment with accrued interest, in each case, subject to income and employment tax withholding. These grants are included in the 2017 Grants of Plan-Based Awards table and the grant date fair value of the awards is included with the NEOs 2017 compensation in the Summary Compensation Table.

The table below details the time-based grants awarded to all eligible employees, including NEOs:

|

| | | | | |

| NEO | RSUs Awarded (Time-Based) | Value at Grant Date(1) | Market Value at Year-End(2) |

| Vincent D. Kelly | 38,554 |

| 799,996 | 603,370 |

|

Michael W. Wallace(3)(4) | 19,891 |

| 354,247 | 311,294 |

|

| Hemant Goel | 12,048 |

| 249,996 | 188,551 |

|

| Bonnie K. Culp-Fingerhut | 4,066 |

| 84,370 | 63,633 |

|

| Thomas G. Saine | 4,969 |

| 103,107 | 77,765 |

|

| |

| (1) | The fair values of the RSUs awarded were calculated at $15.65, the closing price of the Company's common stock on December 30, 2016, the trading day prior to the date of grant. |

| |

| (2) | Market or payout values of the unvested RSUs were based on the target number of RSUs and our closing stock price at December 31, 2017 of $15.65. The RSUs are convertible into shares of the Company’s common stock if the pre-established performance criteria for the 2017-2019 performance period are achieved. |

| |

| (3) | Mr. Wallace became the Chief Financial Officer of the Company in March 2017. In connection with the commencement of his employment, a one-time award of 12,535 RSUs with a grant date fair value of $220,000 was issued to Mr. Wallace on July 17, 2017. This one-time award vests in full at the end of a one year period from the date of grant. |

| |

| (4) | In connection with the commencement of his employment, Mr. Wallace was awarded a pro-rated number of time-based RSUs under the 2017 LTIP. The fair value of which was calculated at $18.25, the closing price of the Company's stock on March 26, 2017, the trading day prior to the grant date, and represented 7,356 RSUs. |

The time-based grants noted in the table above will vest in 3 equal installments on December 31, 2017, 2018 and 2019 based on continued employment with the Company.

Performance-based Vesting Awards - Based on the information from the LRP, the Compensation Committee approved the performance criteria for the 2017 LTIP grant for the 2017-2019 performance period, which performance criteria is measurable, readily reported and requires the coordination and cooperation of all management. The Compensation Committee chose adjusted operating and capital expenses to replace adjusted operating cash flow in order to provide focus on the individual components that adjusted operating cash flow is derived from. Additionally, the Compensation Committee replaced total consolidated revenue with wireless revenue to ensure attention was placed on both the wireless and software revenue streams (software bookings).

The Compensation Committee selected the performance criteria for the 2017 LTIP grant based on the following rationale:

Wireless Revenue – As noted earlier, the Company is in transition from a declining wireless centric revenue base to a growing software centric base as represented by software revenue. As the Company transitions to a software centric base the Compensation Committee believes it is important to focus on the retention of wireless revenues to continue internal funding of research and development projects that it anticipates will fuel long term growth. This performance criteria will reflect a reduction in revenue in comparison to actual results from the prior year given the declining nature of revenues related to those products and services. The Compensation Committee believes that maintaining this revenue stream is a key area of focus as the Company continues its transition into a software centric business. A long term focus on the maintenance of this revenue stream will continue to benefit investors through both capital reallocation opportunities as well as the continued funding of current and future software development efforts.

Adjusted Operating and Capital Expenses – Adjusted Operating and Capital Expenses is defined as operating expenses less depreciation, amortization and accretion expense, less severance, less stock based compensation, plus capital expense (all calculated in accordance with U.S. GAAP). This performance criteria is a non-GAAP measure of the Company's operating expenses. This performance criteria measures the Company’s ability to manage its operations expenses based on parameters established by the Board.

Software Operations Bookings – Software operations bookings represent contractual arrangements to provide software licenses, professional services and equipment sales. These contractual arrangements (bookings) represent future revenue. This performance criteria focuses management on supporting the critical drivers for future growth and implementation of the transition to growth. As the Company accomplishes its transition to overall growth, this performance criteria will generally reflect an increase from the prior year based on the Compensation Committee's understanding of the Company's operations.

The Compensation Committee has determined that wireless revenue, adjusted operating and capital expenses (as defined), and software operations bookings are key elements impacting stockholder value. The Compensation Committee believes that the use of wireless revenue, adjusted operating and capital expenses (as defined), and software operations bookings in both the STIP and LTIP are warranted to motivate management to successfully implement the transition to growth and are aligned with our stockholders interests as follows:

Wireless revenue is the basis for future software growth. The Compensation Committee believes that the use of this metric will focus management on the responsible growth and transition of the Company into a software centric business with a continued focus on remaining debt free and providing itself with internal funding of current and future research and development efforts.

Adjusted operating and capital expenses (as defined) is the non-GAAP measure for the Company's operating expenses. The Compensation Committee believes that the use of this metric will focus management on not only the long-term growth of revenues but on the responsible growth of profitable revenue streams which will continue to generate and provide long-term cash flows and the Company's long-term allocation strategy for stockholder dividends and/or common stock repurchases.

Software operations bookings is the basis for achieving growth. The Compensation Committee's objective is to motivate management to achieve sustainable growth, which would require implementation of the strategies reviewed and approved by the Board (and Compensation Committee) during the review of the LRP.

Payouts are determined based on long-term performance - Management recommended and the Compensation Committee, in its sole discretion, selected employees to be participants in the 2017 LTIP grant.

Under the terms of the performance-based grants, 100% of the target award is in the form of RSUs granted under our 2012 Equity Plan, subject to vesting as described below. Additionally, participants are entitled to DERs with respect to the RSUs to the extent that any cash dividends or cash distributions (regular or otherwise) are paid with respect to our common stock during the 2017-2019 performance period. The DERs are subject to the same vesting restrictions as the RSUs as to howwhich they relate, such that the DERs are paid and are only paid to the extent the applicable performance criteria underlying the RSUs have been attained. Vested RSUs will be settled in the CompanyCompany's common stock and vested DERs will be paid in a lump sum cash payment with accrued interest, in each case, subject to income and employment tax withholding. The Compensation Committee believes that performance-based RSUs link long-term compensation for our executives to our Company’s operational and stock price performance as RSUs are earned only if pre-established performance goals are met and, if earned, are settled in shares of the Company’s common stock upon vesting.

Performance criteria

Similar to the STIP, straight-line interpolation is used to determine payouts for LTIP awards when 1) the actual performance is between the threshold performance level and target performance level or 2) the actual performance is between the target performance level and the maximum performance level. There is no LTIP payout if achievement is below the threshold performance level. Payments under the 2011 LTIP consistedare contingent upon continued employment, though pro rata payments will be made in the event of death or disability based on actual performance at the triggering event date relative to targeted performance measures for each program. Further, if an executive’s employment is involuntarily terminated (other than for cause), the executive will be eligible to receive a pro rata payment of the Company achieving cumulative consolidated revenue of $827.6 millionLTIP for the performance period with a minimum 2014 software revenueyear of $55.8 milliontermination, subject to the execution of an appropriate release and cumulative consolidated OCF of $207.1 million with a minimum consolidated OCF of $28.6 million for 2014. (For purposes of calculating OCF, severance, restructuringother applicable and impairment expenses are excluded.) Revenue and OCF were afforded equal weight in determining attainmentcustomary termination procedures.

The Compensation Committee actively considers the appropriate size of the pay opportunity each year in light of the evolving nature and size of the business. The Compensation Committee determines the threshold, target and maximum payouts for each performance criteria.criterion based on the Compensation Committee's understanding of the Company's LRP and the expectations for 2017. Based on this understanding the Compensation Committee also establishes the relative weighting for each performance criteria with operations bookings afforded the most significant weighting (see "Description of the LTIP Performance Criteria").

The 2011following table summarizes the performance criteria of the 2017 performance-based LTIP awards providedgrant for the 2017-2019 performance period:

|

| | | | |

| 2017 performance-based LTIP Grant |

| Item # | | Weighting | | 2017-2019 Performance Period Criteria(1) |

| 1 | | 20% | | Cumulative Wireless Revenue |

| 2 | | 30% | | Cumulative Adjusted Operating and Capital Expenses(2) |

| 3 | | 50% | | Cumulative Software Operations Bookings(3) |

| Total | | 100% | | |

| |

| (1) | The Compensation Committee selected the performance criteria as key measures in determining stockholder value. The relative weight assigned to each performance measure reflects the judgment of the Compensation Committee as to the importance each measure has to stockholder value. |

| |

| (2) | Operating expenses less depreciation, amortization and accretion expense, less severance, less stock based compensation, plus capital expense (all calculated in accordance with U.S. GAAP). |

| |

| (3) | Software operations bookings represent contractual arrangements to provide software licenses, professional services and equipment sales. These contractual arrangements (bookings) represent future revenue. |

The 2017 LTIP grants provide that the awardgrant will vest and be paid only if the minimum thresholds for the applicable performance criteria for the 2017-2019 performance period are achieved and will be forfeited if the minimum thresholds for the applicable performance criteria for the 2017-2019 performance period are not achieved. The 2011 LTIP does not provide any opportunity to earn awards greater than the target level and recipients of awards are not eligible to receive any partial award payments if the performance targets are achieved at a level of less than 100%. Participants will generally forfeit all rights with respect to RSUs and DERs awarded under the 20112017 LTIP grant if they terminate with cause or voluntarily separate before the payment date.date, subject to employment agreement provisions for our CEO. The 20112017 LTIP awards weregrants will be paid in March 20152020 after filing our 2014 Annual Report on Form 10-K for the year ended December 31, 2019 with the SEC. The Company believes that current disclosure of the amounts of the performance criteria for the 2017-2019 performance period would be competitively harmful by providing the Company’s competition with detailed insight into the Company’s intentions and expectations. The Company will provide the details of the performance criteria for the 2017-2019 performance period upon completion of the 2017-2019 performance period in its 2019 Annual Report on Form 10-K and in its 2020 Proxy Statement.

The following table below details the achievement of the pre-established performance criteria that allowed for payment of the vested RSUs in common stock of the Company in March 2015 after filing our 2014 Annual Report with the SEC.performance-based grants awarded to all eligible employees, including NEOs:

|

| | | | |

| 2011 LTIP Performance Criteria ($ in 000s): | | |

| | Target |

| Achievement |

|

Cumulative Consolidated Revenue (2011 – 2014)(1) | $827,556 | $866,468 |

Cumulative Consolidated Operating Cash Flow (2011 -2014)(2) | 207,110 |

| 222,729 |

|

| Minimum 2014 Software Revenue | 55,767 |

| 67,871 |

|

| Minimum 2014 Operating Cash Flow | 28,569 |

| 38,644 |

|

|

| | | | | |

| NEO | RSUs Awarded (Performance-Based) | Value at Grant Date(1) | Market Value at Year-End(2) |

| Vincent D. Kelly | 38,554 |

| 799,996 | 603,370 |

|

| Hemant Goel | 12,048 |

| 249,996 | 188,551 |

|

Michael W. Wallace(3) | 7,355 |

| 134,229 | 115,106 |

|

| Thomas G. Saine | 4,969 |

| 103,128 | 77,765 |

|

| Bonnie K. Culp-Fingerhut | 4,066 |

| 84,370 | 63,633 |

|

| |

| (1) | Cumulative Consolidated Revenue includes software revenue forThe fair values of the period April 1, 2011 throughRSUs awarded were calculated at $20.75, the closing price of the Company's common stock on December 31, 2014 and excludes30, 2016, the impacttrading day prior to the date of any fair value write down of deferred revenue due to acquisition accounting.grant. |

| |

| (2) | OCF is defined as operating income plus severance and restructuring expenses, plus depreciation, amortization and accretion expenses less purchases of property and equipment all determined in accordance with U.S. GAAP. |

We used the fair-value based method of accounting for the 2011 LTIP. Additional information on the 2011 LTIP can be found in the 2014 Annual Report under “Spok Holdings, Inc. Equity Incentive Plan”. The table below details the grants that were made pursuant to the 2011 LTIP for the NEOs, all of which were made in 2013, except with respect to Mr. Balmforth. The RSUs awarded under the 2011 LTIP vested on December 2014 based on the achievement of the pre-established performance goals. These awards were paid in March 2015.

|

| | | | |

| NEO | Job Title | 2011 LTIP Award ($)(1) | Number of RSUs(2) | Fair Value at Grant Date ($)(3) |

| Vincent D. Kelly | CEO | 3,000,000 | 216,034 | 3,011,787 |

| Shawn E. Endsley | CFO | 281,250 | 24,079 | 270,166 |

| Colin M. Balmforth | President | 599,590 | 50,598 | 566,698 |

| Bonnie K. Culp-Fingerhut | EVP-HR and Administration | 227,908 | 19,512 | 297,857 |

| Thomas G. Saine | CIO | 309,375 | 26,487 | 297,184 |

| |

(1) | The valueMarket or payout values of the initial 2011 LTIP award wasunvested RSUs were based on a multiple of the respective NEO’s annual STIP target and was used to determine the number of RSUs to be awarded toand our closing stock price at December 31, 2017 of $15.65. The RSUs are convertible into shares of the NEO. On July 23, 2013,Company’s common stock if the Compensation Committee andpre-established performance criteria for the Board granted an additional LTIP award to Mr. Kelly totaling $2,100,000. |

| |

(2) | The number of RSUs initially awarded to Mr. Kelly was 77,054 RSUs on January 23, 2013 and an additional 138,980 RSUs were awarded to Mr. Kelly on July 23, 2013 pursuant to his amended employment agreement.2017-2019 performance period are achieved. |

| |